![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()

REVESCO. Revista de Estudios Cooperativos. ARTÍCULOS

e-ISSN: 1985-8031

Thiago de Oliveira Victorino

University

of Brasília (Brasil) and Organization of Brazilian Cooperatives – OCB System

(Brasil) ![]()

![]()

Arthur Gomes Nery

Organization

of Brazilian Cooperatives – OCB System (Brasil) ![]()

![]()

Rodrigo Lima Rangel

Organization

of Brazilian Cooperatives – OCB System (Brasil) ![]()

![]()

https://dx.doi.org/10.5209/REVE.108416 Recibido: 16/10/2025 • Aceptado: 09/01/2026 • Publicado: 29/04/2026

ES Resumen. El sector de la Salud Suplementaria de Brasil incluye una presencia significativa de cooperativas de salud, que representan aproximadamente el 38% del mercado. Estas cooperativas enfrentan desafíos financieros únicos derivados de su complejidad regulatoria, naturaleza mutualista y el conflicto entre los principios cooperativos y las presiones competitivas por la eficiencia económica. A pesar de su importancia, la literatura sobre la predicción de insolvencia para cooperativas es escasa y se basa en gran medida en modelos diseñados para empresas convencionales. Para llenar esta brecha, este artículo utiliza una base de datos de la Agencia Nacional de Salud Suplementaria (ANS) y el Sistema de la Organización de Cooperativas Brasileñas (Sistema OCB) y emplea una regresión logística con regularización Lasso para pronosticar la dificultad financiera en cooperativas de salud. Este enfoque promueve simultáneamente la selección de variables y la regularización del modelo, manteniendo al mismo tiempo su interpretabilidad. El rendimiento general de la clasificación es robusto, con una precisión del 94% y una especificidad del 95%, minimizando con éxito los falsos negativos. Desde el punto de vista académico, la aplicación de la regularización Lasso en este contexto es una contribución metodológica significativa, que llena un vacío en la literatura al integrar estadísticas avanzadas con los desafíos únicos de la gestión de cooperativas de salud. En la práctica, el modelo sirve como un sistema de alerta temprana para gerentes y reguladores, guiando estrategias financieras y prácticas de gestión de riesgos para mejorar la sostenibilidad a largo plazo de estas entidades dentro del sistema de atención médica brasileño.

Palabras clave. Bancarrota, predicción, cooperativa, empresa social, regresión logística, machine learning.

Claves Econlit. G33, I11, C25, C52, P13.

ENG Forecasting financial distress in brazilian healthcare cooperatives: a regularized Logit approach

ENG Abstract. Brazil's Supplemental Health sector includes a significant presence of health cooperatives, which account for approximately 38% of the market. These cooperatives face unique financial challenges from their regulatory complexity, mutualistic nature, and the conflict between cooperative principles and competitive pressures for economic efficiency. Despite their importance, the literature on insolvency prediction for cooperatives is scarce, largely relying on models designed for conventional firms. To fill this gap, this paper makes use of a comprehensive database from the National Supplemental Health Agency (ANS) and the Brazilian Cooperative Organization System (Sistema OCB) and employs a logistic regression with Lasso regularization to forecast financial distress in healthcare cooperatives. This approach simultaneously promotes variable selection and model regularization, while maintaining its interpretability. Overall classification performance is robust, with an accuracy of 94% and a specificity of 95%, successfully minimizing false negatives. Academically, applying Lasso regularization in this context is a significant methodological contribution, filling a literature gap by integrating advanced statistics with the unique challenges of health cooperative management. Practically, the model serves as an early warning system for managers and regulators, guiding financial strategies and risk management practices to enhance the long-term sustainability of these entities within the Brazilian healthcare system.

Keywords. Bankruptcy, forecast, cooperative, social enterprise, logistic regression, machine learning.

Summary. 1. Introduction. 2. Theoretical framework. 3. Methods and materials. 4. Results. 5. Discussion. 6. Concluding remarks. 7. References.

How to cite: Victorino, T.O.; Nery, A.G. & Rangel, R.L. (2026). Forecasting financial distress in brazilian healthcare cooperatives: a regularized Logit approach. REVESCO. Revista de Estudios Cooperativos, 152, e108416. https://dx.doi.org/10.5209/REVE.108416.

Brazil's healthcare system is a hybrid model comprising a public subsystem: Unified Health System (Sistema Único de Saúde - SUS); and a supplementary private sector (Paim et al. 2011). While SUS offers universal healthcare access to all citizens, the supplementary health subsystem provides additional options through private health insurance plans and services.

This supplementary subsystem encompasses private health insurance plan operators, hospitals, clinics, and diagnostic laboratories. As of 2024, 24.5% of Brazilians, or about 52.2 million individuals, were covered by private health plans. This marks an increase from 18.3% in 2002, indicating a growing reliance on private healthcare services[1].

In the supplementary health sector, medical and orthodontic cooperatives play a major role, offering services through networks of affiliated physicians. As such, Unimed is the largest medical cooperative globally, with over 118,000 members, holding 38% of the private health market share[2].

A cooperative is defined as “an autonomous association of persons united voluntarily to meet their common economic, social and cultural needs and aspirations through a jointly owned and democratically controlled enterprise”[3]. As such, cooperatives are built on six main values: self-help, self-responsibility, democracy, equality, equity, and solidarity; and are guided by 73 principles:

1. Voluntary and Open Membership

2. Democratic Member Control

3. Member Economic Participation

4. Autonomy and Independence

5. Education, Training, and Information

6. Cooperation among Cooperatives

7. Concern for Community

Cooperatives, as member-based associations, operate under a "social rationality" that prioritizes social performance and collective benefit, determined by members' participation and commitment (Schneider, 2013). Research suggests cooperatives exhibit anti-cyclical behavior (Birchall and Ketilson, 2009; Zamagni, 2012) and demonstrate greater financial soundness than for-profit counterparts, even offering the same services (Forgione and Migliardo, 2018; Goddard et al., 2008; Hesse and Čihák, 2007).

Despite their mutualistic principles, cooperatives also operate within competitive markets that demand economic efficiency. This creates an inherent tension between serving the mutual interests of members and fulfilling broader social or general-interest missions, a balance that can strain financial resources and strategic focus (Dudka et al. 2024). Furthermore, their member-based governance structures, while democratic, can be susceptible to weaknesses in leadership and decision-making, which are identified as critical vulnerabilities affecting sustainability and resilience of a cooperative (Paraschou et al. 2025).

Within the healthcare sector, cooperatives aim to deliver comprehensive care, encompassing medical, dental, psychological, and patient support. The establishment of Brazilian health cooperatives in the late 1960s represented a direct response by physicians to the commercialization of healthcare by group medicine companies and the exploitation of medical professionals. Fundamentally, these cooperatives prioritize generating employment and income for their physician members (Gulak et al., 2024).

Despite its growth, Brazilian supplementary health subsystem operates under significant financial pressure. An important constraint is the regulatory framework governing premium adjustments. For individual and family health plans, the National Agency of Supplementary Health (ANS) defines an annual ceiling for price readjustments, calculated via the Índice de Reajuste dos Planos Individuais (IRPI). In contrast, adjustments for collective health plans, which represent 83.3% of the market, are subject to commercial negotiation between operators and contracting companies, offering greater flexibility.

Against these revenue constraints, operational costs rise consistently. Factors include the incorporation of new medical technologies, the demographic pressure of an aging population and beneficiary base, and increases in the price of medical and hospital inputs. This misalignment between regulated or negotiated revenue and growing costs contributes to high claims ratios, where expenses can exceed collected premiums.

Additional sectoral challenges intensify this pressure. Market concentration advantages larger operators, while legal disputes over coverage add financial uncertainty. Although ANS interventions aim to maintain stability, the financial vulnerability of operators, particularly smaller cooperatives, persists.

Despite its importance, the literature addressing insolvency in cooperatives remains scarce. Existing studies predominantly focus on bankruptcy prediction models tailored to conventional firms, overlooking the structural and operational specificities of cooperatives. Notable among these specificities are differentiated corporate governance, mutualistic aspects, and the inherent conflict between cooperative principles and competitive pressure for economic efficiency. This gap underscores the need for innovative methodological approaches tailored to the sector's peculiarities.

Thus, this article’s objective is to develop a model to forecast insolvency risk in supplemental health cooperatives providing a practical and effective tool for managing insolvency risks. To do so, we employ a logistic regression, widely recognized as a robust tool for modelling binary dependent variables, and incorporate the Lasso regularization technique.

Amid rising challenges, tools like this are indispensable for promoting organizational sustainability, and the combination of a rigorous methodological approach, high-quality data, and a focus on cooperative specificities reinforces the strategic role of cooperatives in the Supplemental Health subsystem and points to promising pathways for enhancing risk management in the sector.

Including this introduction, this article is organized as follows: Chapter 2 presents the theoretical framework revolving around insolvency, Chapter 3 presents the methods’ description and databases, Chapter 4 presents the results, Chapter 5 presents the discussion and Chapter 6 presents the concluding remarks.

2.1. Bankruptcy Forecasting

Emerging in the late 1960s, bankruptcy and insolvency risk analysis are key areas of economic and financial research but still face a challenging landscape due to diverse industry benchmarks and their complex interactions with financial, legal, and economic factors (Clement, 2020; Gholampoor and Asadi, 2024). Altman (1968) and Beaver (1966) are recognized as the pioneers of modern bankruptcy forecasting, with the influential Z-Score, utilizing discriminant analysis and financial ratios. Twelve years later, Ohlson (1980) significantly advanced the field by introducing logistic regression for financial distress forecasting. Since then, corporate bankruptcy literature has seen an exponential growth, accompanied by increasing sophistication in forecasting models.

The financial viability of healthcare organizations represents a critical pillar of public welfare. Unlike corporate failures in other sectors, the bankruptcy of healthcare firms and health systems imposes relevant social costs, imposing a meaningful impact on local communities, often resulting in restricted access, higher cost, and lower quality of care available (Beauvais et al. 2023).

Despite this high social cost, the domain of healthcare corporate failure forecast remains underexplored, with limited literature concerning financial forecasting models and knowledge detailing the specific factors associated with hospital bankruptcy (Beauvais et al. 2023). This limitation surely impacts the non-profit and public health spheres, where financial distress is also characterized as a "relatively underexplored area" globally, despite the frequent occurrence of financial failures (Karakolias, 2025).

Compounding this issue for cooperatives, this extensive academic focus on Investor-Owned Firms imposes an inherent bias in established failure prediction methodologies. Classic models, such as those developed by Altman and Ohlson, are designed primarily to forecast statutory insolvency, the legal event of bankruptcy (e.g., Chapter 11 or 7 filing), driven by financial collapse (Keating et al., 2005). Regulatory and financial liquidation mechanisms as the dependent variable are often unsuitable for organizations whose legal status, governance structure, and objectives deviate from profit maximization.

As such, "very few studies have been devoted to predicting failures of cooperative societies" (Mateos-Ronco and Mas, 2011; Sarsale, 2020). This neglect is highlighted by the observation that applying established IOF models, such as the Altman model, is considered "rare" among cooperatives (Sarsale, 2020), and often inadequate.

Even though few studies examine insolvency risks in cooperatives and non-profit sectors, we highlight some important developments. Forgione and Migliardo (2018) analyze small Italian cooperative banks during a financial crisis through a Logit approach, emphasizing the importance of bank capital as a predictor of failure. Their findings diverge from for-profit banking models, highlighting that traditional risk factors such as non-performing loans and liquidity are less predictive for cooperatives. Braga et al. (2006) apply the Cox Proportional Hazards Model to Brazilian credit unions, determining that general liquidity, salary expenses, and the loan/equity ratio are the most effective indicators of insolvency risk. In a similar spirit, Bressan et al. (2011) in an attempt to adapt the PEARLS system indicators to the Brazilian context, estimate the insolvency risk of credit cooperatives affiliated with the Brazilian Credit Cooperatives System (Sicoob) through a Logit model, highlighting the importance of key indicators from the original PEARLS system such as Protection, Effective Financial Structure, Asset Quality, and Rates of Return and Costs.

Research on Spanish cooperatives indicates that size is a critical determinant of financial distress, with small cooperatives often exhibiting the weakest financial ratios despite micro-enterprises showing lower external dependence (del Campo and López, 2013). Methodologically, applications of fuzzy logic to assess credit cooperatives in Ecuador demonstrate alternative approaches for evaluating financial health, capturing the gradational nature of risk that traditional binary models may overlook (Diaz Córdova et al., 2017).

Naaman et al. (2021) compare risk-taking behaviors between shareholder-owned banks and member-owned credit unions in the U.S., revealing that banks tend to assume higher risks, although state regulatory oversight narrows this gap. These findings align with Duncan (2021), who provides a practical framework for small banks and credit unions to conduct risk assessments and strengthen their financial resilience.

From a methodological perspective, logistic regression has become the most popular method to forecast bankruptcy (Cheraghali and Molnár, 2024; Jones et al., 2017). However, as popular as it might be, authors such as Begley et al. (1996) argued that methods based on Altman (1968) and Ohlson (1980) had become inaccurate especially due to their limitations when considering nonlinear relationships among independent variables (Barboza and Altman, 2024; Khemakhem and Boujelbene, 2018; Shi and Li, 2019), as is often the case in financial distressed firms. In this context, machine learning methods have emerged as an option to the now classic Logit, providing more accurate predictions with a wider set of tools (Brenes et al., 2022; Gavurova et al., 2022; Kim et al., 2022; Lombardo et al., 2022; Zhao et al., 2023).

Along with these new approaches, a critical challenge arises: interpretability. Machine learning methods often function as "black boxes," making it difficult to understand the mathematical processes driving each model. This lack of transparency can cast doubt on their usability and raise concerns among stakeholders who require transparency for decision. We are faced with the accuracy vs. interpretability dilemma.

To address this dual challenge—the lack of cooperative-specific models and the interpretability limits of machine learning—we incorporate the Lasso regularization technique into the logistic regression. This approach offers advantages, particularly in handling multicollinearity while maintaining model interpretability. Lasso performs variable selection by shrinking less relevant coefficients to zero, reducing overfitting and enhancing the model’s predictive power, especially with high-dimensional financial data.

Unlike black-box models, Lasso retains the intuitive structure of logit regression but enhances its performance by selecting the most relevant predictors and reducing noise. This allows for higher accuracy without sacrificing explainability, ensuring that decision-makers, regulators, and cooperative managers can still understand and justify the model’s outputs. The ability to pinpoint key financial indicators driving insolvency risk makes Lasso a powerful tool in this context, providing both actionable insights and reliable predictions.

2.2. Brazilian Health System

Brazil's healthcare system is a hybrid model anchored by two main components. The public component is the Unified Health System (SUS), established by the 1988 Constitution to guarantee universal and free access to comprehensive healthcare for all citizens, funded primarily by taxes.

Operating in parallel is the supplementary private health subsystem, which is strictly regulated by the National Agency of Supplementary Health (ANS) and functions through health plan operators (operadoras de planos de saúde). These operators function as financial and administrative intermediaries: they sell health plans, contract and manage provider networks (hospitals, clinics, professionals), and process claims.

The main categories of health plan operators are:

· Medical and Odontological Cooperatives (e.g., Unimed): Nonprofit entities where physicians are members and owners. Unimed is the world's largest medical cooperative system, holding about 38% of the private market share.

· Group Medicine: Typically for-profit corporations that often own their own healthcare facilities, creating vertically integrated networks. Examples include Hapvida, which is the largest group medicine operator in Brazil with 16% of the market, along with other important firms such as Amil;

· Health Insurance Companies (e.g., Bradesco Saúde, SulAmérica): Offer plans that reimburse expenses or provide network access, accounting for around 13% of the market.

· Self-Managed Plans: Nonprofit operators serving only a defined group, such as public employees or company dependents.

The Brazilian supplementary health market comprises two main segments: individual/family plans and collective (primarily corporate) plans. Individual plans, which make up 16.7% of the market, are subject to stricter regulatory price controls. In contrast, collective plans, representing 83.3% of the market, allow for greater flexibility in negotiations between health operators and contracting companies.

These operators compete directly for the same customers, with their financial success driven by risk pooling, cost management, and governance, as their revenues derive almost exclusively from private contracts.

In terms of relevance, Brazil's private supplementary healthcare subsystem serves 52.2 million people through 669 health plan operators, while odontological assistance serves 34.8 million people through 320 health plan operators[4], and cooperatives are a relevant part of both sectors.

In medical assistance, Unimed represents the largest network of medical cooperatives globally. It is a confederative system composed of 340 independent cooperatives (singulars) operating under a unified brand. While these cooperatives share branding and strategic guidelines, they possess financial and operational autonomy. Collectively, Unimed holds around 38% of the private market share, serving 21 million beneficiaries (beneficiários). This confederated network is owned by approximately 118,000 physician-members and employs over 158,000 administrative collaborators, creating a combined workforce of over 276,000 individuals[5].

2.3. The Emergence of Healthcare Cooperatives in Brazil

The contemporary structure of the Brazilian supplementary health sector, described above, is the result of a distinct historical evolution. Before the structural reforms of the late 1980s, the Brazilian health system was characterized by a deep fragmentation. Between the 1930s and 1980s, the system operated primarily through three segments: first, there was the strictly private sector, where individuals paid directly for services or utilized limited private plans; second, the social security system was linked to the Institutos de Aposentadoria e Pensões (IAPs), which provided health care only to formal sector workers and their dependents; the third segment comprised a rudimentary public health system (Ferreira, 2022). This highly segmented structure was incapable of meeting the rapidly increasing social demands for health access (Ferreira, 2022).

The rise of the military dictatorship in 1964 coincided with a period of economic expansion, particularly in the industrial sector, throughout the 1960s and 1970s (Ferreira, 2022). This economic growth, however, disproportionately benefited the wealthiest portion of the population (Paim et al., 2011) and suppressed broader social demands for a universal public system, as the government prioritized economic growth beneficial to large industries (Paim et al., 2011; Ferreira, 2022), while allocating few resources to the Ministry of Health, hindering its ability to develop public health initiatives (Polignano, 2001). It was a clear option for capital-intensive, curative medicine, financed primarily through contributions from workers to the social security system (Polignano, 2001), designed to provide the conditions for the monetization of health needs.

The defining structural shift that immediately preceded the emergence of Unimed was the unification of the Institutos de Aposentadoria e Pensões. This unification process culminated in the creation of the Instituto Nacional de Previdência Social (INPS) in 1967. This administrative reform substantially increased the number of contributors and, consequently, the number of beneficiaries eligible for medical care, but it also overloaded the existing medical system (Polignano, 2001). Within this capacity crisis, the strategic choice made by the government was to prioritize directing public resources toward the private initiative (Polignano, 2001). By expanding the number of beneficiaries while simultaneously directing public funds toward private providers, the state sanctioned the market space for new, complementary private entities to absorb the strain from the overwhelmed social security system (Assumpção, 2023).

In a professional counter-reaction to the centralizing bureaucracy of the INPS, on December 18, 1967, the União dos Médicos (Unimed) was founded in Santos. The purpose of its creation was to form an organization that guaranteed the dignity of physicians and patients; that is, physicians being able to practice their profession freely, and patients having access to quality medicine and the possibility of choosing a medical professional they trust. The creation of the medical work cooperative was an alternative reaction by the medical class, tied to the labor union of medical professionals, to the proliferation of commercial companies, which showed an interest in making health a source of profit, with aggressive exploitation of medical professionals (Albuquerque, 2012).

The cooperative movement that began with Unimed in 1967 represented one professional and organizational response to the limitations of Brazil's inefficient health system. The definitive political and structural response would emerge from the broad social mobilization of the Reforma Sanitária (Sanitary Reform). This vision was incorporated into the 1988 Constitution, which, in Article 196, declared health as a universal right and mandated the creation of SUS. Regulated by Laws No. 8.080/1990 and 8.142/1990, SUS was founded on the principles of universality, integrality, and equity, unifying the previously fragmented public and social security structures into a single, publicly funded system organized across federal, state, and municipal levels (Paim et al., 2011).

2.4. Cooperative Governance and Regulation in Brazil

Within this hybrid system, comprising both private and public healthcare, Unimed (and all Brazilian cooperatives for that matter) operates under the National Policy of Cooperativism, which establishes the legal regime for cooperative societies through Law No. 5.764/1971, distinguishing them as non-profit entities where the person, rather than capital, is the central element (Arts. 3 and 4).

A critical aspect of this legal framework is the governance structure it imposes. Under Article 38, the General Assembly of members serves as the supreme decision-making body. However, the law mandates a strict requirement for the administrative bodies: according to Article 47, the Board of Directors or Executive Board must be composed exclusively of associated members elected by the Assembly. In the specific context of health cooperatives (which function as worker cooperatives), this implies that strategic governance is, by law, in the exclusive domain of medical professionals.

While Article 48 permits the hiring of non-member technical managers or CEOs for operational roles, the ultimate authority, including the approval of financial accounts and strategic direction, remains with the physician-members. This arrangement creates a distinct governance environment where the strategic controllers are also the primary service providers. The impact of such governance structures on financial stability remains a subject of debate. As noted in a systematic review by Jamaluddin et al. (2023), the literature regarding cooperative board composition and leadership yields contradictory results, leaving a gap in understanding how these specific governance mechanisms influence risk management and solvency.

This unique cooperative structure, when operating in healthcare market as insurers, functions within a specific regulatory architecture enforced by the National Agency of Supplementary Health (ANS) that seeks to ensure the stability of operators and protect beneficiaries. Its founding instrument is Law No. 9.656/1998 and the Normative Resolution No. 518/2022 is especially important to this study, as it establishes corporate governance practices with an emphasis on internal controls and risk management to improve the solvency of health plan operators. This regulation forms part of a comprehensive oversight mechanism that includes licensing requirements, mandatory financial reporting, and regulatory audits. A key enforcement tool under RN 518 is the mandatory monitoring of a set of financial ratios, such as net margin, return on assets, and sinistrality, to provide a standardized assessment of an operator's economic and financial health. This framework aims to ensure insurers maintain sufficient financial reserves to meet their obligations, thereby protecting consumers and promoting market stability.

However, while monitoring a defined set of individual financial ratios, as mandated by regulations such as RN 518, provides a baseline, this compliance-based approach may offer an incomplete picture of an operator's true financial health. Academic literature strongly suggests that a more precise assessment of solvency requires understanding not just the isolated values of these ratios, but how they interact with and complement one another within an integrated analytical framework.

A key limitation of examining ratios in isolation is that they provide a static snapshot of financial health at a single point in time, derived from balance sheets and income statements (Seretidou et al. 2025). Ratios like net margin or return on assets (ROA) are important but can miss the dynamic operation of a firm. Therefore, moving beyond a checklist of isolated metrics towards an integrative analysis is the main object of this study. For a cooperative health plan operator, whose solvency is essential to fulfill its social mission, adopting a comprehensive analytical perspective is an important component of robust, forward-looking governance and risk management.

3.1. Logistic Regression

Logistic regression is a statistical method used to model the probability that an observation belongs to a particular class. In the case of binary classification, it estimates the probability that 𝑌 belongs to class 1 given a set of independent variables 𝑋 via a sigmoid function:

![]()

where ![]() is the predicted probability of insolvency,

is the predicted probability of insolvency, ![]() is the intercept,

is the intercept, ![]() are the coefficients of the set of independent variables

are the coefficients of the set of independent variables ![]() and

and ![]() is the Euler’s number. The model is estimated using maximum

likelihood estimation (MLE), where coefficients are chosen to maximize the

likelihood of the observed data.

is the Euler’s number. The model is estimated using maximum

likelihood estimation (MLE), where coefficients are chosen to maximize the

likelihood of the observed data.

3.2. Lasso Regularization

Lasso is a type of regularization applied to

regression models, including logit regression, to improve predictive

performance and feature selection. It adds an ![]() penalty term to the log-likelihood function:

penalty term to the log-likelihood function:

where ![]() is the standard negative log-likelihood from logistic regression,

is the standard negative log-likelihood from logistic regression, ![]() is the Lasso penalty, which shrinks coefficients to zero,

effectively performing variable selection and

is the Lasso penalty, which shrinks coefficients to zero,

effectively performing variable selection and ![]() is a tuning parameter that controls the strength of the

regularization. To define

is a tuning parameter that controls the strength of the

regularization. To define ![]() , we opt for the K-fold cross-validation (Hastie et al., 2009), with 10 folds.

, we opt for the K-fold cross-validation (Hastie et al., 2009), with 10 folds.

3.3. Data and Variables

We collected our database directly from the Brazilian regulatory agency ANS, through the TabNet service, spanning 10 years (2014-2023) of yearly accounting data for 339 Brazilian healthcare cooperatives, in a total of 3,397 observations after data processing. As an important sidenote, the temporal scope of our dataset encompasses the economic and operational disruptions caused by the COVID-19 pandemic, which manifested in the sector through volatile claims patterns, deferred elective procedures, and shifts in patient utilization. Consequently, the financial ratios in our sample already reflect the shock and subsequent recovery of this period. By training on data that contains a significant, real-world stressor, we can assess if the model is able to identify coherent signals of financial distress that are relevant not only in stable conditions but also during and after a major systemic crisis. This ensures that the predictive framework is calibrated for resilience and is applicable to the volatile economic reality in which healthcare cooperatives operate.

The available data required significant processing, as it is published in a long format, with various missing values. The following steps were followed to build the final database:

· The financial data for each year was bound row-wise;

· The bound data was pivoted (transposed) to a wide format, where each row is a health plan operator and each column is a financial variable;

· Healthcare cooperatives with no assets, no liabilities, or no revenue were removed.

To classify the healthcare cooperative as financially distressed/insolvent, we followed preceding literature and defined it as the inability to meet financial obligations (Barboza and Altman, 2024). Thus, for this research, Insolvency is: (i) EBITDA less than financial expenses OR (ii) negative net worth.

The selection of independent variables was based on two key criteria: availability in the dataset and their importance in prior studies (Altman et al., 2017; Barboza and Altman, 2024; Rezende et al., 2017; Sayari and Mugan, 2017).

Table 1. Summary Statistics of Independent Variables

|

Variable |

Desc. |

N |

Mean |

Std. Dev. |

Min |

Pctl. 25 |

Pctl. 75 |

Max |

|

EndT |

Total Debt/Assets |

3397 |

0.55 |

0.29 |

0.014 |

0.4 |

0.65 |

6.5 |

|

LiqC |

Current Assets/Current Liabilities |

3397 |

2.3 |

2.5 |

-93 |

1.4 |

2.6 |

33 |

|

Tes |

Treasury |

3397 |

0.43 |

0.21 |

-0.95 |

0.28 |

0.59 |

0.99 |

|

ML |

Net Margin |

3397 |

0.04 |

0.11 |

-2.5 |

0.0078 |

0.072 |

1.1 |

|

CGAT |

Working Capital/Assets |

3397 |

0.29 |

0.26 |

-4.8 |

0.14 |

0.46 |

0.89 |

|

CSDIV |

Share Capital/Total Debt |

3397 |

0.42 |

0.75 |

-0.65 |

0.14 |

0.46 |

18 |

|

PTAT |

Liabilities/Assets |

3397 |

0.55 |

0.29 |

0.014 |

0.4 |

0.65 |

6.5 |

|

IAT |

Revenue/Assets |

3397 |

1.9 |

0.86 |

0.012 |

1.4 |

2.3 |

12 |

|

logING |

Log of Revenue |

3397 |

18 |

2 |

12 |

16 |

19 |

23 |

|

MargOP |

Operational Margin |

3397 |

0.024 |

0.13 |

-4.3 |

-0.0056 |

0.06 |

1 |

|

Sinis |

Sinistrality |

3397 |

0.75 |

0.82 |

-2 |

0.63 |

0.84 |

38 |

|

Kanitz |

Kanitz Score |

3397 |

8.5 |

18 |

-808 |

5.6 |

11 |

188 |

|

Ind |

NetWorth/Assets |

3397 |

0.45 |

0.29 |

-5.5 |

0.35 |

0.6 |

0.99 |

|

COMBA |

ANS Comba |

3397 |

0.89 |

12 |

-648 |

0.89 |

1 |

48 |

|

COMB |

ANS Comb |

3397 |

1.1 |

8.6 |

-1 |

0.94 |

1 |

502 |

|

ROA |

Return on Assets |

3397 |

0.053 |

0.15 |

-3.1 |

0.014 |

0.11 |

0.93 |

|

Alavac |

Current Liabilities/Net Worth |

3397 |

1.6 |

31 |

-70 |

0.42 |

1.2 |

1769 |

Source: Authors

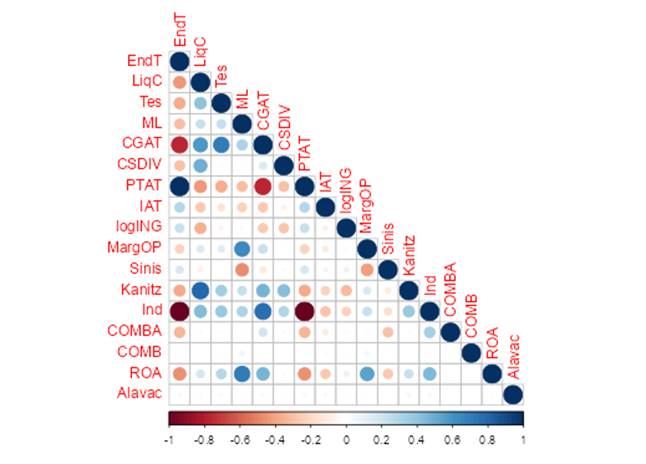

(fig.1) Correlogram

Importantly, while the data is longitudinal, the model is built on a pooled basis as there is evidence that forecasting models can benefit from pooling when there is “not much heterogeneity in the model parameters” (Mark & Sul, 2012).

From this final database, we were able to design the study case. The database was split into two samples: training and test. The training sample is intended to calibrate the model and the test sample was used to assess the model’s accuracy. The training sample was formed by the data from 2014 to 2022. The test sample was formed by data from 2023 and it was held out as a test sample to evaluate the model's predictive performance on unseen, recent data, providing an out-of-sample validation.

The quality of each model will be assessed by a set of measures, commonly used in financial studies, based on the confusion matrix. Each of these measures will be computed for the training and test samples.

Table 2. Confusion Matrix

|

Actual Negative (0) |

Actual Positive (1) |

|

|

Predicted Negative (0) |

True Negative (TN) |

False Negative (FN) |

|

Predicted Positive (1) |

False Positive (FP) |

True Positive (TP) |

Source: Authors

Accuracy:

![]()

Specificity:

![]()

Sensitivity:

![]()

Balanced Accuracy:

![]()

AUC:

![]()

The predicted probability of insolvency resulting from the regularized logit model is a value between 0 and 1, however, to assess model quality, this probability must be converted into a binary outcome (e.g., "insolvent" or "not insolvent") by selecting a cutoff threshold.

One might approach this problem with a naïve cutoff of 0.5, where probabilities above this threshold are classified as "insolvent". While this approach is intuitive, it assumes that the costs of Type I (1 - Sensitivity) and Type II (1 – Specificity) errors are equal, which is not the case in bankruptcy forecasting (Barboza and Altman, 2024). In practice, the costs of classification errors are asymmetric. A false positive (erroneously flagging a solvent cooperative as distressed one) incurs a manageable cost, as it may trigger heightened internal scrutiny, unnecessary testing, or additional reporting to regulators. While suboptimal, these measures are corrective and precautionary and can be absorbed by a healthy operator. They do not result in the catastrophic loss of stakeholder confidence and disruption of healthcare services that a false negative would incur.

Thus, we opt for a more nuanced approach, setting a cost function that explicitly accounts for the consequences of false positives and false negatives. We assign a higher cost to Type II errors (false negatives) of 5, and a lower cost for Type I errors (false positives) of 1. This ensures that the model prioritizes the detection of truly insolvent firms, even at the expense of increasing false positives:

![]()

where ![]() represents the true bankruptcy outcome for observation,

represents the true bankruptcy outcome for observation, ![]() and

and ![]() represents the corresponding predicted

classification.

represents the corresponding predicted

classification.

![]() equals

1 if the condition within the braces is true and 0 otherwise. A false positive incurs

a cost of 1, while a false negative incurs a cost of 5.

equals

1 if the condition within the braces is true and 0 otherwise. A false positive incurs

a cost of 1, while a false negative incurs a cost of 5.

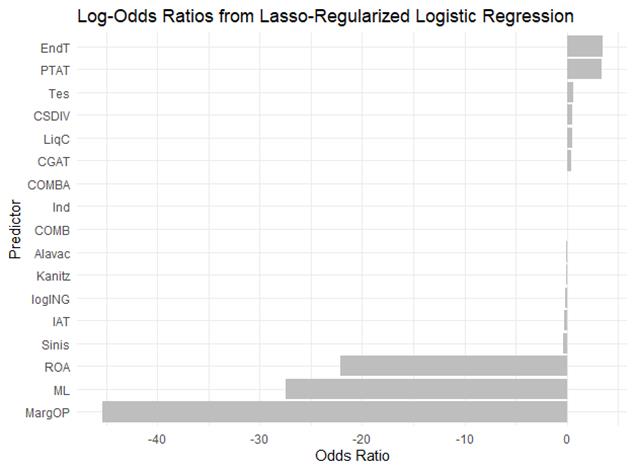

Table 3 presents the Lasso Regularization

results from the Logit Regression model.

Table 3. Estimated Coefficients from Lasso Regularization

|

Variable |

Coefficient |

% Change Odds |

|

EndT |

3.4410 |

3.5008 |

|

PTAT |

3.0752 |

3.1230 |

|

Tes |

0.6859 |

0.6883 |

|

CSDIV |

0.5229 |

0.5243 |

|

LiqC |

0.4909 |

0.4922 |

|

CGAT |

0.4130 |

0.4138 |

|

COMBA |

0.0106 |

0.0106 |

|

Ind |

- |

- |

|

COMB |

- |

- |

|

Alavac |

-0.0030 |

-0.0030 |

|

Kanitz |

-0.0849 |

-0.0848 |

|

logING |

-0.1351 |

-0.1350 |

|

IAT |

-0.2405 |

-0.2402 |

|

Sinis |

-0.2974 |

-0.2969 |

|

ROA |

-25.6189 |

-22.6004 |

|

ML |

-31.5107 |

-27.0289 |

|

MargOP |

-59.0611 |

-44.6011 |

Source: Authors

Each predictor’s coefficient represents the change in the log-odds of the outcome for a one-unit increase in that predictor. By exponentiating these coefficients, we obtain the odds ratios, which provide an intuitive measure of how the odds of the outcome change with variations in the predictors. An odds ratio greater than one indicates that an increase in the predictor raises the odds of the event occurring, while an odds ratio less than one suggests a protective effect.

With Lasso regularization, we

incorporate the ![]() penalty to the regression model. This

penalty forces some of the coefficients to shrink to zero, making the result

sparser, more interpretable and less prone to overfitting and

multicollinearity. Although the interpretation of the log-odds and odds ratios

remains conceptually the same in a lasso-regularized model, we warn that the

estimates are “shrunk” compared to an unpenalized model.

penalty to the regression model. This

penalty forces some of the coefficients to shrink to zero, making the result

sparser, more interpretable and less prone to overfitting and

multicollinearity. Although the interpretation of the log-odds and odds ratios

remains conceptually the same in a lasso-regularized model, we warn that the

estimates are “shrunk” compared to an unpenalized model.

In concrete, from the resulting coefficients in Table 2, we highlight that for every 0.01 increase in Operational Margin, the odds of insolvency are reduced by 44.6%, suggesting that even small improvements in Operational Margin are associated with substantially lower odds of insolvency. Further, a 0.01 rise in total debt ratio (EndT) is associated with a 3.5% increase in the odds of insolvency. Figure 2 presents the odds ratios of each considered variable. Its interpretation is: for every 0.01 increase in the financial ratio, x-axis presents the change in the odds of insolvency.

(fig.2) Odds Ratios of the Logit Lasso Regularized Regression

This balance of accuracy and interpretability is particularly important, as we are able to deliver a robust and more accurate risk assessment, while presenting a transparent indication of how each variable affects insolvency risk, effectively supporting data-driven decisions.

Consistent with Gholampoor and Asadi (2024) and Mushonga (2018), our findings show ROA as a significant insolvency predictor, highlighting the importance of efficient asset utilization for healthcare firm financial stability. Echoing Ngumo et al. (2020), operational efficiency, herein represented by Net Margin and Operational Margin, have a significant effect on financial sustainability. Also, higher margins can improve cash flow, in congruence with the findings of Jace et al. (2022) that Cash Flow negatively affects insolvency risk. However, unlike Jace et al. (2022), we find that Liquidity and Working Capital do not substantially impact the odds of insolvency.

Regarding Total Debt, it is not incorporated in the popular sets of predictor variables used in Altman's Z-score but is a rather important leverage ratio in our study that reveal the proportion of a firm's assets that are financed. As stated by Reis et al. (2021), Total Debt is the variable that most impacts ANS’s decision to submit healthcare operators into the special regime of extrajudicial liquidation.

Lastly, Size, represented by the log of the revenue, barely affects insolvency risk, but shows the expected sign: the larger the revenue, lower the insolvency risk.

Moving beyond individual predictors, we present a comparative profile of solvent versus distressed cooperatives, using the complete dataset (2014-2023). This analysis clarifies the financial characteristics that differentiate successful entities. As indicated by their shrunk-lasso coefficients, cooperatives that remain solvent are typically distinguished by superior operational efficiency (significantly higher Operational and Net Margins) and more conservative financial leverage (a lower Total Debt ratio).

In contrast, distressed cooperatives exhibit weaker margins and higher reliance on debt. For instance, the mean Operational Margin for the solvent group was 6,4% compared to -3,8% for the distressed group, while the mean Total Debt ratio showed an inverse pattern at 48% versus 65%.

Table 4. Summary Statistics by Solvency Status

|

Insolvent? |

0 |

1 |

||||

|

Variable |

N |

Mean |

SD |

N |

Mean |

SD |

|

EndT |

2076 |

0.48 |

0.17 |

1321 |

0.65 |

0.39 |

|

LiqC |

2076 |

2.6 |

2.1 |

1321 |

1.8 |

1.3 |

|

Tes |

2076 |

0.47 |

0.2 |

1321 |

0.37 |

0.22 |

|

ML |

2076 |

0.078 |

0.07 |

1321 |

-0.02 |

0.13 |

|

CGAT |

2076 |

0.35 |

0.2 |

1321 |

0.2 |

0.32 |

|

CSDIV |

2076 |

0.43 |

0.82 |

1321 |

0.39 |

0.61 |

|

PTAT |

2076 |

0.48 |

0.17 |

1321 |

0.65 |

0.39 |

|

IAT |

2076 |

1.8 |

0.73 |

1321 |

2.1 |

1 |

|

logING |

2076 |

18 |

1.8 |

1321 |

18 |

2.1 |

|

MargOP |

2076 |

0.064 |

0.065 |

1321 |

-0.038 |

0.17 |

|

Sinis |

2076 |

0.7 |

0.36 |

1321 |

0.81 |

1.2 |

|

Kanitz |

2076 |

11 |

7.7 |

1321 |

6.5 |

9 |

|

Ind |

2076 |

0.52 |

0.17 |

1321 |

0.35 |

0.39 |

|

COMBA |

2076 |

1 |

5.3 |

1321 |

0.69 |

18 |

|

COMB |

2076 |

1.2 |

11 |

1321 |

1 |

0.19 |

|

ROA |

2076 |

0.11 |

0.064 |

1321 |

-0.039 |

0.2 |

|

Alavac |

2076 |

0.83 |

1.5 |

1321 |

2.8 |

49 |

Source: Authors

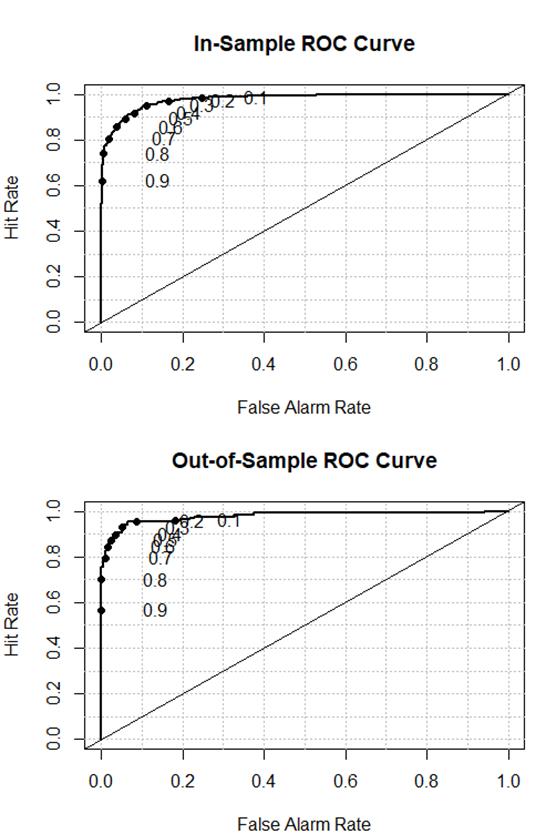

For model quality, Table 5, Table 6 and Figure 3 present the main model quality statistics:

Table 5. Quality of Model Statistics

|

Statistic |

In-Sample |

Out-of-Sample |

|

Accuracy |

0.8968 |

0.9423 |

|

Sensitivity |

0.8572 |

0.9298 |

|

Specificity |

0.9637 |

0.9534 |

|

Balanced Accuracy |

0.9104 |

0.9416 |

|

AUC ROC |

0.9772 |

0.9784 |

Source: Authors

Table 6. In and Out of Sample Confusion Matrixes

|

In-Sample Confusion Matrix |

||

|

Reference |

||

|

Prediction |

0 |

1 |

|

0 |

1633 |

41 |

|

1 |

272 |

1087 |

|

Out-of-Sample Confusion Matrix |

||

|

Reference |

||

|

Prediction |

0 |

1 |

|

0 |

159 |

9 |

|

1 |

12 |

184 |

Source: Authors

(fig.3) In and Out of Sample ROC Curves

When looking at the ROC Curves and the resulting Area Under the Curve, the model shows a high discrimination ability, with high values of sensitivity (true negative rate) and specificity (true positive rate) simultaneously. Typically, logistic regression models’ AUC fall into the range of 0.65 to 0.80 (Hilbe, 2016). Our model specification shows a significantly higher AUC – 0.97. Taking studies on credit and bank cooperatives as benchmark, as there is no previous study on insolvency forecast of healthcare cooperatives, the AUC values range from 0.78 (Calabrese and Giudici, 2015), to 0.926 (Mare, 2015), and many other intermediate values (Altman et al., 2017; Fiordelisi and Mare, 2013; Forgione and Migliardo, 2018; Porath, 2006).

Moreover, it is interesting to notice that the quality of model’s statistics remains mostly unchanged in and out of sample, indicating that there is no overfitting in our modelling. Further, Specificity is above 95% in both training and test samples, indicating that our cost function approach to determine the ideal cutoff value is adequate.

Forecasting insolvency remains a great challenge in financial research (Clement, 2020), mostly restricted to banks and listed companies (Barboza and Altman, 2024). Yet, insolvency forecasting in healthcare sector carries substantial weight due to its far-reaching financial repercussions (Gholampoor and Asadi, 2024). In this context, the method discussed in this research offers a significant proactive governance tool for the OCB System, with robust results. The Brazilian Cooperative Organization System is the central, national-level entity that represents all cooperative sectors in Brazil, recognized by law as the primary institutional representative of the movement (Law No. 5.764/1971).

By identifying high-risk cooperatives through early detection of financial vulnerabilities, the model enables OCB to tailor its governance support programs more strategically. Rather than applying a one-size-fits-all approach, OCB can focus its resources and training on those cooperatives that require immediate attention. This targeted strategy not only improves the effectiveness of governance initiatives but also ensures that early-warning indicators are monitored and acted upon in a timely manner.

At the organizational level, the model's key predictors can translate into actionable governance tools. A cooperative board of directors can institutionalize the monitoring of critical variables identified by the Lasso regularization, such as Operational Margin (MargOP) and the Total Debt ratio (EndT), by establishing them as primary metrics in a financial health dashboard. Setting internal policy thresholds for these indicators, for instance, triggering a mandatory review if the Operational Margin falls below a certain level or if leverage exceeds a predefined limit, transforms the model from a diagnostic tool into a mechanism for proactive governance. This approach empowers boards to move beyond retrospective analysis of financial statements and engage in forward-looking risk management.

Leadership development programs can also benefit from this approach. By identifying cooperatives at risk of insolvency, OCB is in a position to offer tailored training aimed at improving financial management, internal controls, and overall risk management practices. Specialized workshops and advisory services can be developed based on these insights, helping cooperatives to enhance their financial discipline and take corrective actions before financial challenges escalate.

In addition, the model serves as a bridge between cooperatives and regulatory bodies such as ANS. Early identification of at-risk cooperatives allows OCB to collaborate closely with regulators to align intervention strategies, ensuring that cooperatives receive the necessary support to comply with regulatory requirements. This synergy between OCB, cooperatives, and regulators promises more effective oversight and ultimately better outcomes for the sector.

From a regulatory perspective, the predictive framework offers a foundation for a more dynamic and risk-based supervision system. The ANS could leverage the model to develop a tiered supervisory approach, where cooperatives are categorized based on their predicted risk of distress. Operators consistently flagged as high-risk over consecutive periods could be placed under an "enhanced monitoring" regime, subject to more frequent reporting requirements, targeted audits focusing on governance and liquidity management, and mandatory submission of corrective action plans. Conversely, cooperatives with persistently low-risk scores could benefit from a "light-touch" supervision track, reducing administrative burden. This data-driven stratification, based on the principles of the Responsive Regulation, would allow the regulator to optimize the allocation of its oversight resources, concentrating efforts where they are most needed to prevent market disruption and protect beneficiaries, thereby enhancing the overall stability and efficiency of the supplementary health sector.

Ultimately, the goal of the model is to foster the long-term sustainability of cooperatives within Brazil’s healthcare system. By leveraging quality data and adequate predictive techniques, the model not only advances the field of insolvency forecasting in a traditionally under-researched area but also provides practical, actionable insights that contribute to more resilient financial governance practices.

This study addressed the critical gap in forecasting insolvency in healthcare cooperatives by developing a novel approach that integrates logit regression with Lasso regularization. The model’s exceptional out-of-sample performance—94% accuracy and 95% specificity—underscores its robustness in distinguishing solvent from insolvent entities, thereby offering a reliable tool for proactive risk management. These results not only surpass existing benchmarks but also validate the efficacy of combining advanced statistical methods with high-quality regulatory data from the ANS, which plays a pivotal role in ensuring transparency and consistency.

While this model focuses on financial predictors, it is critical to recognize that the cost of a cooperative's failure is not merely financial. The disruption to healthcare access for beneficiaries represents an important social cost. This model aims to provide the earliest possible warning using audited financial data, so that stakeholders can intervene to avert both the economic and the more profound social consequences of financial failure.

As such, from a practical standpoint, the model serves as a valuable early warning system for cooperatives, regulators, and stakeholders. By identifying key financial and governance determinants of insolvency, it empowers decision-makers to implement preemptive measures, align financial strategies with sustainability goals, and refine risk management frameworks. This is particularly vital in a sector with escalating costs, regulatory pressures, and the dual mandate of balancing mutualistic principles with economic efficiency. The ANS’s rigorous oversight and data accessibility further amplify the model’s utility, demonstrating how regulatory frameworks can synergize with academic research to enhance sector-wide stability.

Academically, this study breaks new ground by adapting Lasso regularization to the unique context of health cooperatives. While Lasso is well-established in finance, its application here addresses structural specificities of cooperatives, such as governance dynamics and mutualistic objectives, which are often overlooked in conventional bankruptcy models. This methodological innovation sets a precedent for future studies to explore hybrid techniques that prioritize interpretability without compromising accuracy, thereby bridging the gap between theoretical research and practical challenges.

A logical and valuable extension, as suggested in the literature on comparative institutional analysis, would be to contrast these findings with a model for traditional, investor-owned health insurers. Such a comparison could reveal whether the mutualistic principles and governance structure of cooperatives lead to distinctly different financial failure pathways or confer comparative resilience. This might be an interesting path to future studies.

While effective, using only financial ratios may not capture the unique institutional characteristics of cooperatives, such as their governance model, member participation intensity, or social performance. These factors, central to cooperative identity, are inherently difficult to quantify and are not systematically captured in the regulatory financial data used here. Future research could aim to develop standardized metrics for these qualitative aspects and test their incremental predictive power when combined with financial data, building upon the baseline model established in this work.

Also, future research could expand this framework to other cooperative sectors, such as agriculture or credit unions, to test its generalizability. Exploring ensemble methods or explainable AI (XAI) could also enhance model performance, although sacrificing transparency when predicting is more important than explaining.

In conclusion, this study transcends academic inquiry by delivering a pragmatic tool that fortifies the strategic role of cooperatives in Brazil’s healthcare ecosystem. By harmonizing methodological rigor, regulatory collaboration, and sector-specific insights, it charts a path toward resilient cooperative management, ensuring these entities continue to serve as pillars of equitable healthcare access in an increasingly complex landscape.

The authors declare no conflict of interest.

Victorino, T.O: Conceptualization, Methodology, Data curation, Formal analysis, Project administration, Writing – original draft, Writing – review & editing.

Nery, A.G: Conceptualization, Data curation, Writing – review & editing.

Rangel, R.L: Conceptualization, Data curation, Writing – review & editing.

The data supporting the findings of this study are available in the following Repository: https://www.ans.gov.br/anstabnet/.

During the preparation of this work, the author(s) used Gemini and Claude in order to proofread the final version, checking for minor typographical mistakes, and improve overall readability. After using this tool, the author(s) reviewed and edited the content as necessary, assuming full responsibility for the content of the publication.

Albuquerque, A. (2012). Unimed, 45 anos: uma história de paixão pelo Cooperativismo Médico. São Paulo: Unimed do Brasil.

Altman, E.I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy, The Journal of Finance, JSTOR, Vol. 23 No. 4, pp. 589–609.

Altman, E.I., Iwanicz‐Drozdowska, M., Laitinen, E.K. and Suvas, A. (2017). Financial distress prediction in an international context: A review and empirical analysis of Altman’s Z‐score model, Journal of International Financial Management & Accounting, Wiley Online Library, Vol. 28 No. 2, pp. 131–171.

Assumpção, B. G. D. (2023). A contribuição da sociedade cooperativa no acesso da população aos serviços de saúde: o caso da Unimed–cooperativa de trabalho médico.

Barboza, F. and Altman, E. (2024). Predicting financial distress in Latin American companies: A comparative analysis of logistic regression and random forest models, The North American Journal of Economics and Finance, Elsevier, Vol. 72, p. 102158.

Beauvais, B., Ramamonjiarivelo, Z., Betancourt, J., Cruz, J., & Fulton, L. (2023). The predictive factors of hospital bankruptcy—an exploratory study. In Healthcare (Vol. 11, No. 2, p. 165). MDPI.

Beaver, W.H. (1966). Financial ratios as predictors of failure, Journal of Accounting Research, JSTOR, pp. 71–111.

Begley, J., Ming, J. and Watts, S. (1996). Bankruptcy classification errors in the 1980s: An empirical analysis of Altman’s and Ohlson’s models, Review of Accounting Studies, Springer, Vol. 1, pp. 267–284.

Birchall, J. and Ketilson, L.H. (2009). Resilience of the Cooperative Business Model in Times of Crisis, International Labour Organisation.

Braga, M.J., Fully Bressan, V.G., Colosimo, E.A. and Bressan, A.A. (2006). Investigating the solvency of Brazilian credit unions using a proportional hazard model, Annals of Public and Cooperative Economics, Wiley Online Library, Vol. 77 No. 1, pp. 83–106.

Brenes, R.F., Johannssen, A. and Chukhrova, N. (2022). An intelligent bankruptcy prediction model using a multilayer perceptron, Intelligent Systems with Applications, Elsevier, Vol. 16, p. 200136.

Bressan, V.G.F., Braga, M.J., Bressan, A.A. and de Andrade Resende Filho, M. (2011). Uma aplicação do sistema PEARLS às cooperativas de crédito brasileiras, Revista de Administração, Elsevier, Vol. 46 No. 3, pp. 258–274.

Calabrese, R. and Giudici, P. (2015). Estimating bank default with generalised extreme value regression models, Journal of the Operational Research Society, Taylor & Francis, Vol. 66 No. 11, pp. 1783–1792.

Cheraghali, H. and Molnár, P. (2024). SME default prediction: A systematic methodology-focused review, Journal of Small Business Management, Taylor & Francis, Vol. 62 No. 6, pp. 2847–2905.

Clement, C. (2020). Machine learning in bankruptcy prediction–a review, Journal of Public Administration, Finance and Law, Editura Tehnopress, No. 17, pp. 178–196.

del Campo, J. I., & López, S. M. (2013). El tamaño como elemento determinante de la insolvencia en las sociedades cooperativas: estudio a partir de los procesos concursales. REVESCO. Revista de Estudios Cooperativos, Nº 111, pp. 90-107.

Díaz Córdova, J. F., Coba Molina, E., & Navarrete, P. (2017). Lógica difusa y el riesgo financiero. Una propuesta de clasificación de riesgo financiero al sector cooperativo. Contaduría y administración, 62(SPE5), 1670-1686.

Dudka, A., Magnani, N., & Koukoufikis, G. (2024). Analysing perspectives on capital, mutual, and general interest: A comparative study of energy cooperatives in Belgium and in Italy. Energy Research & Social Science, 116, 103665.

Duncan, P. (2021). A methodology for enterprise-wide risk assessment in small banks and credit union, Journal of Money Laundering Control, Emerald Publishing Limited, Vol. 24 No. 2, pp. 374–395.

Ferreira, M. (2022). Health financialization in Brazil: some evidence in the hospital sector. Économie et institutions, (30-31).

Fiordelisi, F. and Mare, D.S. (2013). Probability of default and efficiency in cooperative banking, Journal of International Financial Markets, Institutions and Money, Elsevier, Vol. 26, pp. 30–45.

Forgione, A.F. and Migliardo, C. (2018). Forecasting distress in cooperative banks: The role of asset quality, International Journal of Forecasting, Elsevier, Vol. 34 No. 4, pp. 678–695.

Gavurova, B., Jencova, S., Bačík, R., Miskufova, M. and Letkovský, S. (2022). Artificial intelligence in predicting the bankruptcy of non-financial corporations, Oeconomia Copernicana, Nicolaus Copernicus University.

Gholampoor, H. and Asadi, M. (2024). Risk Analysis of Bankruptcy in the US Healthcare Industries Based on Financial Ratios: A Machine Learning Analysis, Journal of Theoretical and Applied Electronic Commerce Research, MDPI, Vol. 19 No. 2, pp. 1303–1320.

Goddard, J., McKillop, D. and Wilson, J.O.S. (2008). What drives the performance of cooperative financial institutions? Evidence for US credit unions, Applied Financial Economics, Taylor & Francis, Vol. 18 No. 11, pp. 879–893.

Gulak, D., Moreira, V.R. and Ferraresi, A.A. (2024). Social performance indicators in Brazilian health cooperatives, Social Enterprise Journal, Emerald Publishing Limited.

Hastie, T., Tibshirani, R., Friedman, J.H. and Friedman, J.H. (2009), The Elements of Statistical Learning: Data Mining, Inference, and Prediction, Vol. 2, Springer.

Hesse, H. and Čihák, M. (2007). Cooperative banks and financial stability, IMF working paper.

Hilbe, J.M. (2016). Practical Guide to Logistic Regression, Chapman and Hall/CRC, DOI: 10.1201/b18678.

Jace, K., Koumanakos, D. and Tsagkanos, A. (2022). Bankruptcy Prediction in Social Enterprises, Journal of Social Entrepreneurship, Routledge, Vol. 13 No. 2, pp. 205–220, doi: 10.1080/19420676.2020.1763438.

Jamaluddin, F., Saleh, N. M., Abdullah, A., Hassan, M. S., Hamzah, N., Jaffar, R., ... & Embong, Z. (2023). Cooperative governance and cooperative performance: A systematic literature review. Sage Open, 13(3), 21582440231192944.

Jones, S., Johnstone, D. and Wilson, R. (2017). Predicting Corporate Bankruptcy: An Evaluation of Alternative Statistical Frameworks, Journal of Business Finance & Accounting, Vol. 44 No. 1–2, pp. 3–34, DOI: 10.1111/jbfa.12218.

Karakolias, S. (2025). Rethinking financial distress in public healthcare: evidence from Greek hospitals' governance attributes. Frontiers in Public Health, 13, 1690901.

Keating, E. K., Fischer, M., Gordon, T. P., & Greenlee, J. S. (2005). Assessing financial vulnerability in the nonprofit sector. Available at SSRN 647662.

Khemakhem, S. and Boujelbene, Y. (2018). Support vector machines for credit risk assessment with imbalanced datasets, International Journal of Data Mining, Modelling and Management, Inderscience Publishers (IEL), Vol. 10 No. 2, pp. 171–187.

Kim, H., Cho, H. and Ryu, D. (2022). Corporate bankruptcy prediction using machine learning methodologies with a focus on sequential data, Computational Economics, Springer, Vol. 59 No. 3, pp. 1231–1249.

Lombardo, G., Pellegrino, M., Adosoglou, G., Cagnoni, S., Pardalos, P.M. and Poggi, A. (2022). Machine learning for bankruptcy prediction in the American stock market: dataset and benchmarks, Future Internet, MDPI, Vol. 14 No. 8, p. 244.

Mare, D.S. (2015). Contribution of macroeconomic factors to the prediction of small bank failures, Journal of International Financial Markets, Institutions and Money, Elsevier, Vol. 39, pp. 25–39.

Mark, N., & Sul, D. (2012). When Are Pooled Panel‐Data Regression Forecasts of Exchange Rates More Accurate than the Time‐Series Regression Forecasts?. Handbook of exchange rates, 265-281.

Mateos Ronco, A. M., & López Mas, Á. (2011). Developing a business failure prediction model for cooperatives: Results of an empirical study in Spain. African Journal of Business Management, 5(26), 10565-10576.

Mushonga, M. (2018). The efficiency and sustainability of co-operative financial institutions in South Africa, Stellenbosch: Stellenbosch University.

Naaman, C., Magnan, M., Hammami, A. and Yao, L. (2021). Credit unions vs. commercial banks, who takes more risk?, Research in International Business and Finance, Elsevier, Vol. 55, p. 101340.

Ngumo, K.S., Collins, K.W. and David, S.H. (2020). Determinants of financial performance of microfinance banks in Kenya, ArXiv Preprint ArXiv:2010.12569.

Ohlson, J.A. (1980). Financial ratios and the probabilistic prediction of bankruptcy, Journal of Accounting Research, JSTOR, pp. 109–131.

Paim, J., Travassos, C., Almeida, C., Bahia, L., & Macinko, J. (2011). The Brazilian health system: history, advances, and challenges. The Lancet, 377(9779), 1778-1797.

Paraschou, M., Sergaki, P., Kalogeras, N., Nastis, S. A., & Staboulis, C. (2025). Agricultural Cooperatives: Roadblocks to Achieving Sustainability. Sustainability, 17(17), 8012.

Polignano, M. V. (2001). História das políticas de saúde no Brasil: uma pequena revisão. Cadernos do Internato Rural-Faculdade de Medicina/UFMG, 35, 01-35.

Porath, D. (2006). Estimating probabilities of default for German savings banks and credit cooperatives, Schmalenbach Business Review, Springer, Vol. 58, pp. 214–233.

Reis, T.A., da Silva Macedo, M.A. and da Costa Marques, J.A.V. (2021). Desempenho econômico-financeiro e as decisões de instauração de regimes especiais no setor de saúde suplementar brasileiro, Revista Contemporânea de Contabilidade, Vol. 18 No. 48, pp. 156–174.

Rezende, F.F., Montezano, R.M. da S., Oliveira, F.N. de and Lameira, V. de J. (2017). Predicting financial distress in publicly-traded companies, Revista Contabilidade & Finanças, SciELO Brasil, Vol. 28, pp. 390–406.

Sarsale, M. (2020). Measuring Financial Health of Selected Cooperatives in an ASEAN Province Using Altman Model. Journal of Educational and Human Resource Development (JEHRD), 8, 80-93.

Sayari, N. and Mugan, C.S. (2017). Industry specific financial distress modeling, BRQ Business Research Quarterly, SAGE Publications Sage UK: London, England, Vol. 20 No. 1, pp. 45–62.

Schneider, J.O. (2013). A Doutrina do Cooperativismo: Análise do Alcance, do Sentido e da Atualidade dos seus Valores, Princípios e Normas nos Tempos Atuais, Cadernos Gestão Social, Vol. 3 No. 2 SE-Fórum 'Cooperativismo e Gestão de Empreendimentos Cooperativos', pp. 251–273.

Seretidou, D., Billios, D., & Stavropoulos, A. (2025). Integrative Analysis of Traditional and Cash Flow Financial Ratios: Insights from a Systematic Comparative Review. Risks, 13(4), 62.

Shi, Y. and Li, X. (2019). An overview of bankruptcy prediction models for corporate firms: A systematic literature review, Intangible Capital, OmniaScience, Vol. 15 No. 2, pp. 114–127.

Zamagni, V.N. (2012). Interpreting the roles and economic importance of cooperative enterprises in a historical perspective, Journal of Entrepreneurial and Organizational Diversity, Vol. 1 No. 1, pp. 21–36.

Zhao, Z., Li, D. and Dai, W. (2023). Machine-learning-enabled intelligence computing for crisis management in small and medium-sized enterprises (SMEs), Technological Forecasting and Social Change, Elsevier, Vol. 191, p. 122492.

[1] https://www.gov.br/ans/pt-br/acesso-a-informacao/perfil-do-setor/dados-gerais, accessed on December 2nd, 2025.

2 https://www.gov.br/ans/pt-br/acesso-a-informacao/perfil-do-setor/dados-gerais, accessed on December 2nd, 2025.

[3] https://ica.coop/en/cooperatives/cooperative-identity, accessed on December 2nd, 2025.

[4] https://www.gov.br/ans/pt-br/arquivos/acesso-a-informacao/perfil-do-setor/dados-e-indicadores-do-setor/publicacoes/Panorama_Saude_Suplementar_Ed_08_mar_2025_r07.pdf, accessed on December 2nd, 2025.

[5] https://www.unimed.coop.br/site/sistema-unimed, accessed on December 2nd, 2025.